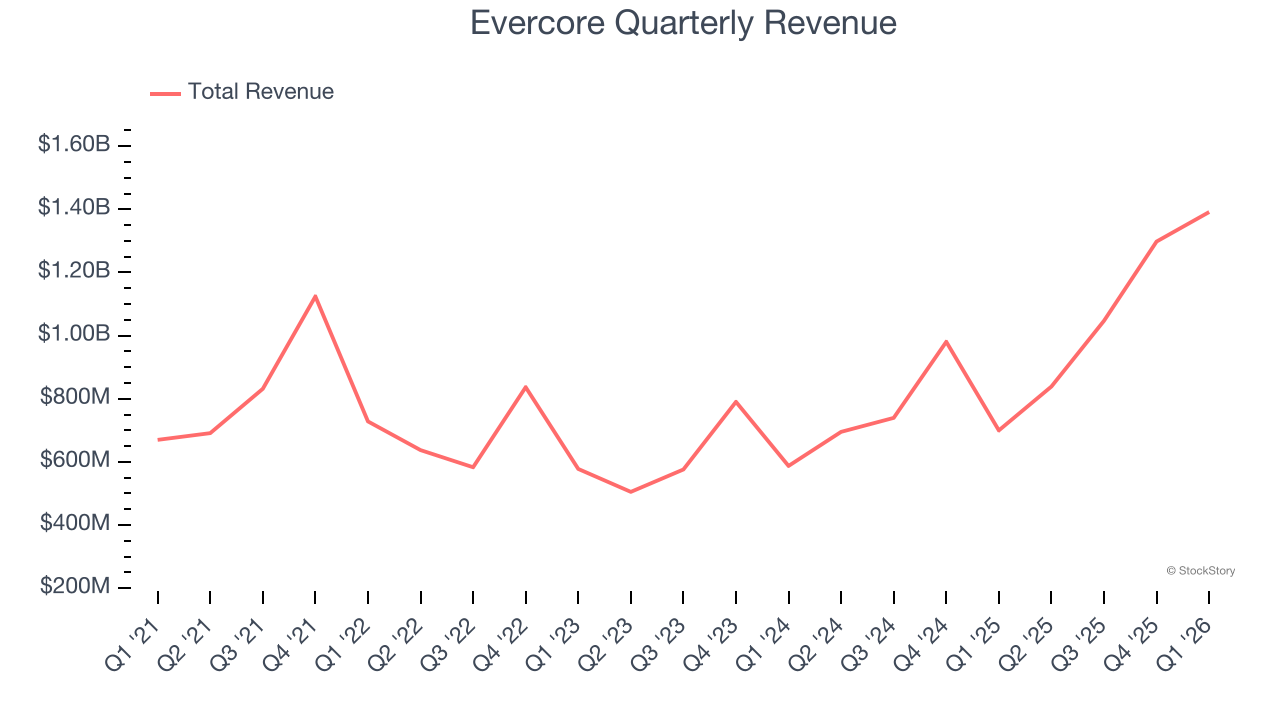

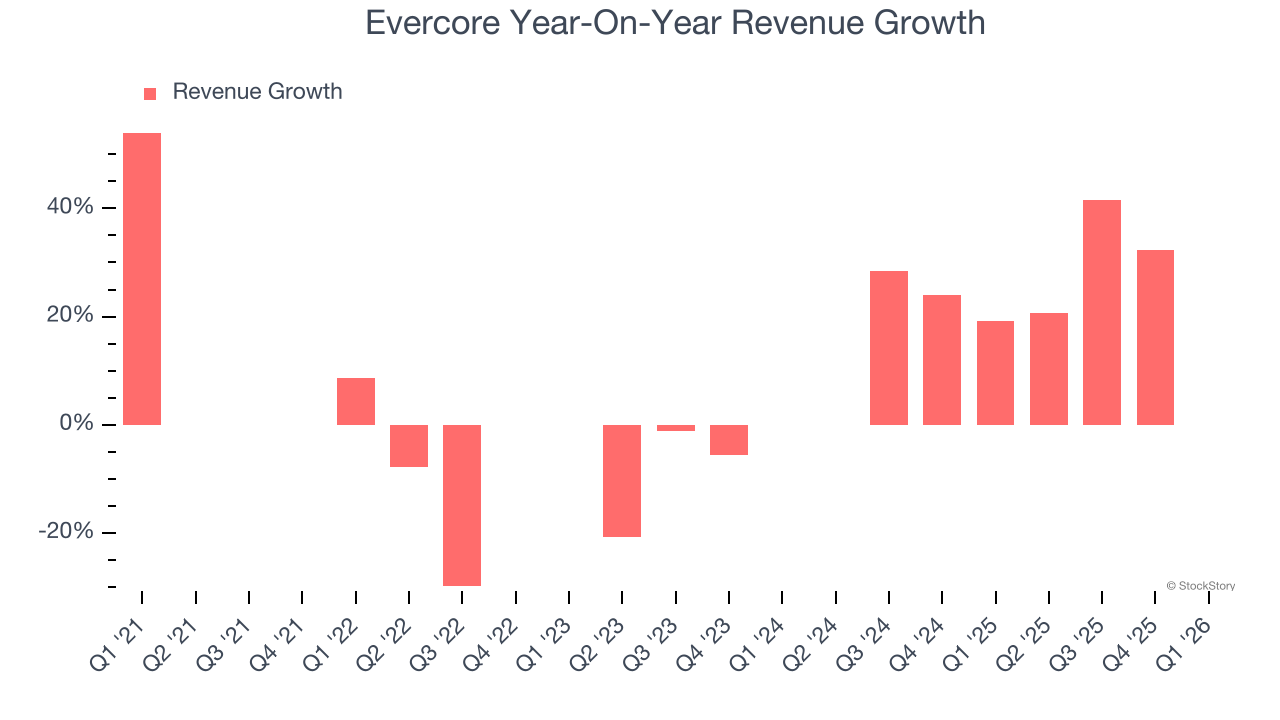

Investment banking firm Evercore (NYSE:EVR) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 98.8% year on year to $1.39 billion. Its non-GAAP profit of $7.53 per share was 38.8% above analysts’ consensus estimates.

Is now the time to buy Evercore? Find out by accessing our full research report, it’s free.

Evercore (EVR) Q1 CY2026 Highlights:

- Revenue: $1.39 billion vs analyst estimates of $1.20 billion (98.8% year-on-year growth, 15.8% beat)

- Pre-tax Profit: $331.8 million (23.8% margin)

- Adjusted EPS: $7.53 vs analyst estimates of $5.43 (38.8% beat)

- Market Capitalization: $13.49 billion

Company Overview

Founded in 1995 as a boutique advisory firm focused on independence and client trust, Evercore (NYSE:EVR) is an independent investment banking firm that provides strategic advisory, capital markets, and wealth management services to corporations, financial sponsors, and high-net-worth individuals.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Evercore’s 12.3% annualized revenue growth over the last five years was solid. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Evercore’s annualized revenue growth of 36.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Evercore reported magnificent year-on-year revenue growth of 98.8%, and its $1.39 billion of revenue beat Wall Street’s estimates by 15.8%.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Key Takeaways from Evercore’s Q1 Results

It was good to see Evercore beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $340.51 immediately after reporting.

Is Evercore an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).